import numpy as np

import matplotlib.pyplot as plt

import pandas as pd

from sklearn.preprocessing import RobustScaler

plt.style.use("bmh")

import ta

from datetime import timedelta

from keras.models import Sequential

from keras.layers import LSTM, Dense, Dropout

df = pd.read_csv("USDTRY=X.csv")

df['Date'] = pd.to_datetime(df.Date)

# Setting the index

df.set_index('Date', inplace=True)

# Dropping any NaNs

df.dropna(inplace=True)

# Adding all the indicators

df = ta.add_all_ta_features(df, open="Open", high="High", low="Low", close="Close", volume="Volume", fillna=True)

# Dropping everything else besides 'Close' and the Indicators

df.drop(['Open', 'High', 'Low', 'Adj Close', 'Volume'], axis=1, inplace=True)

# Checking the new df with indicators

print(df.shape)

# Only using the last 1000 days of data to get a more accurate representation of the current climate

df = df.tail(1000)

# Scale fitting the close prices separately for inverse_transformations purposes later

close_scaler = RobustScaler()

close_scaler.fit(df[['Close']])

# Normalizing/Scaling the Data

scaler = RobustScaler()

df = pd.DataFrame(scaler.fit_transform(df), columns=df.columns, index=df.index)

# Plotting the Closing Prices

df['Close'].plot(figsize=(16,5))

plt.title("Satis Fiyati")

plt.ylabel("Fiyat(olcekli)")

# plt.show()

def split_sequence(seq, n_steps_in, n_steps_out):

"""

Splits the multivariate time sequence

"""

# Creating a list for both variables

X, y = [], []

for i in range(len(seq)):

# Finding the end of the current sequence

end = i + n_steps_in

out_end = end + n_steps_out

# Breaking out of the loop if we have exceeded the dataset's length

if out_end > len(seq):

break

# Splitting the sequences into: x = past prices and indicators, y = prices ahead

seq_x, seq_y = seq[i:end, :], seq[end:out_end, 0]

X.append(seq_x)

y.append(seq_y)

return np.array(X), np.array(y)

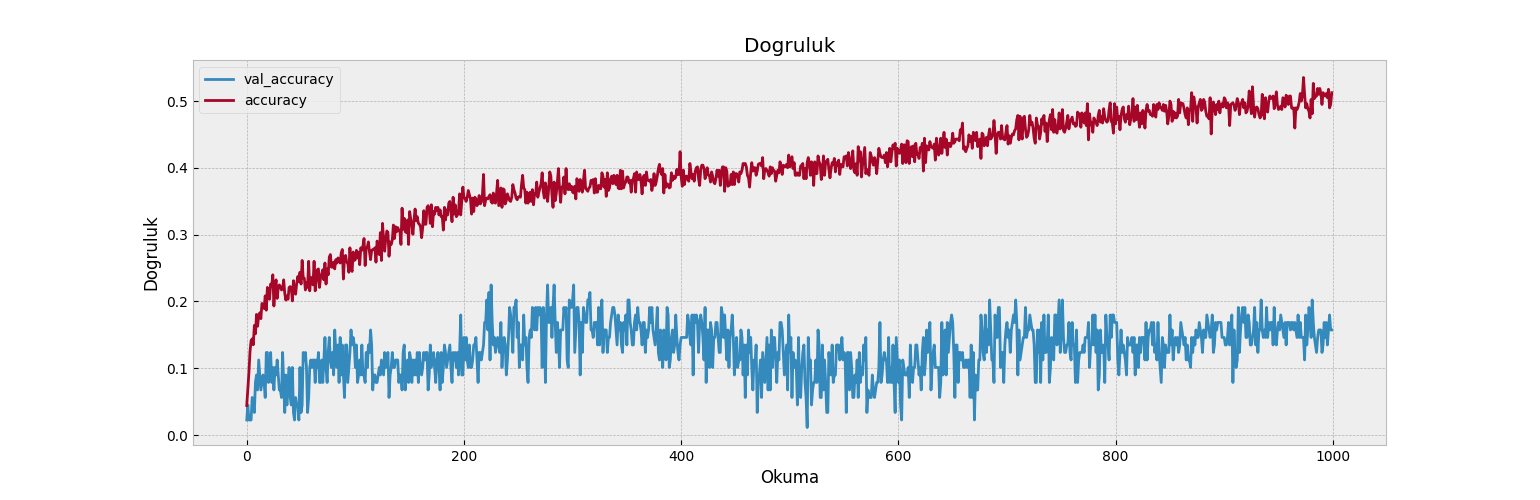

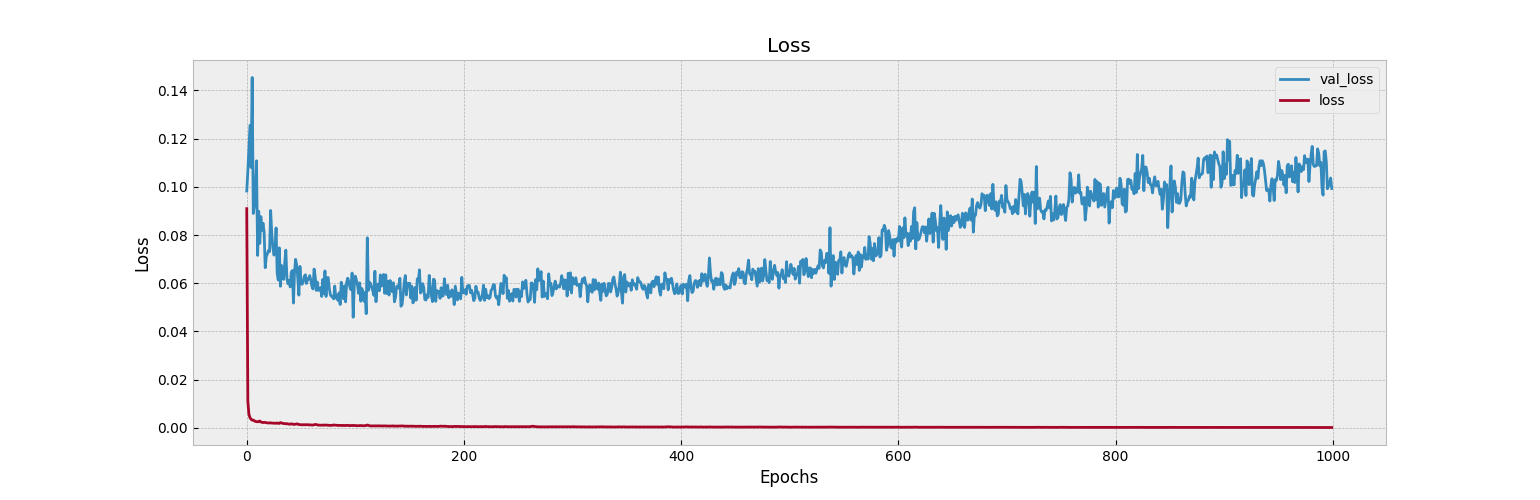

def visualize_training_results(results):

"""

Plots the loss and accuracy for the training and testing data

"""

history = results.history

plt.figure(figsize=(16,5))

plt.plot(history['val_loss'])

plt.plot(history['loss'])

plt.legend(['val_loss', 'loss'])

plt.title('Loss')

plt.xlabel('Epochs')

plt.ylabel('Loss')

plt.show()

plt.figure(figsize=(16,5))

plt.plot(history['val_accuracy'])

plt.plot(history['accuracy'])

plt.legend(['val_accuracy', 'accuracy'])

plt.title('Dogruluk')

plt.xlabel('Okuma')

plt.ylabel('Dogruluk')

plt.show()

def layer_maker(n_layers, n_nodes, activation, drop=None, d_rate=.5):

"""

Creates a specified number of hidden layers for an RNN

Optional: Adds regularization option - the dropout layer to prevent potential overfitting (if necessary)

"""

# Creating the specified number of hidden layers with the specified number of nodes

for x in range(1,n_layers+1):

model.add(LSTM(n_nodes, activation=activation, return_sequences=True))

# Adds a Dropout layer after every Nth hidden layer (the 'drop' variable)

try:

if x % drop == 0:

model.add(Dropout(d_rate))

except:

pass

def validater(n_per_in, n_per_out):

"""

Runs a 'For' loop to iterate through the length of the DF and create predicted values for every stated interval

Returns a DF containing the predicted values for the model with the corresponding index values based on a business day frequency

"""

# Creating an empty DF to store the predictions

predictions = pd.DataFrame(index=df.index, columns=[df.columns[0]])

for i in range(1, len(df)-n_per_in, n_per_out):

# Creating rolling intervals to predict off of

x = df[-i - n_per_in:-i]

# Predicting using rolling intervals

yhat = model.predict(np.array(x).reshape(1, n_per_in, n_features))

# Transforming values back to their normal prices

yhat = close_scaler.inverse_transform(yhat)[0]

# DF to store the values and append later, frequency uses business days

pred_df = pd.DataFrame(yhat,

index=pd.date_range(start=x.index[-1]+timedelta(days=1),

periods=len(yhat),

freq="B"),

columns=[x.columns[0]])

# Updating the predictions DF

predictions.update(pred_df)

return predictions

def val_rmse(df1, df2):

"""

Calculates the root mean square error between the two Dataframes

"""

df = df1.copy()

# Adding a new column with the closing prices from the second DF

df['close2'] = df2.Close

# Dropping the NaN values

df.dropna(inplace=True)

# Adding another column containing the difference between the two DFs' closing prices

df['diff'] = df.Close - df.close2

# Squaring the difference and getting the mean

rms = (df[['diff']]**2).mean()

# Returning the sqaure root of the root mean square

return float(np.sqrt(rms))

# How many periods looking back to learn

n_per_in = 30

# How many periods to predict

n_per_out = 10

# Features

n_features = df.shape[1]

# Splitting the data into appropriate sequences

X, y = split_sequence(df.to_numpy(), n_per_in, n_per_out)

# Instatiating the model

model = Sequential()

# Activation

activ = "tanh"

# Input layer

model.add(LSTM(90,

activation=activ,

return_sequences=True,

input_shape=(n_per_in, n_features)))

# Hidden layers

layer_maker(n_layers=2,

n_nodes=30,

activation=activ,

drop=1,

d_rate=.1)

# Final Hidden layer

model.add(LSTM(90, activation=activ))

# Output layer

model.add(Dense(n_per_out))

# Model summary

model.summary()

# Compiling the data with selected specifications

model.compile(optimizer='adam', loss='mse', metrics=['accuracy'])

res = model.fit(X, y, epochs=2, batch_size=32, validation_split=0.1)

visualize_training_results(res)

# Transforming the actual values to their original price

actual = pd.DataFrame(close_scaler.inverse_transform(df[["Close"]]),

index=df.index,

columns=[df.columns[0]])

# Getting a DF of the predicted values to validate against

predictions = validater(n_per_in, n_per_out)

# Printing the RMSE

print("RMSE:", val_rmse(actual, predictions))

# Plotting

plt.figure(figsize=(16,6))

# Plotting those predictions

plt.plot(predictions, label='Tahmin edilen')

# Plotting the actual values

plt.plot(actual, label='Gerçek')

plt.title(f"Tahmin ve Gercek Fiyat")

plt.ylabel("Fiyat")

plt.legend()

plt.show()

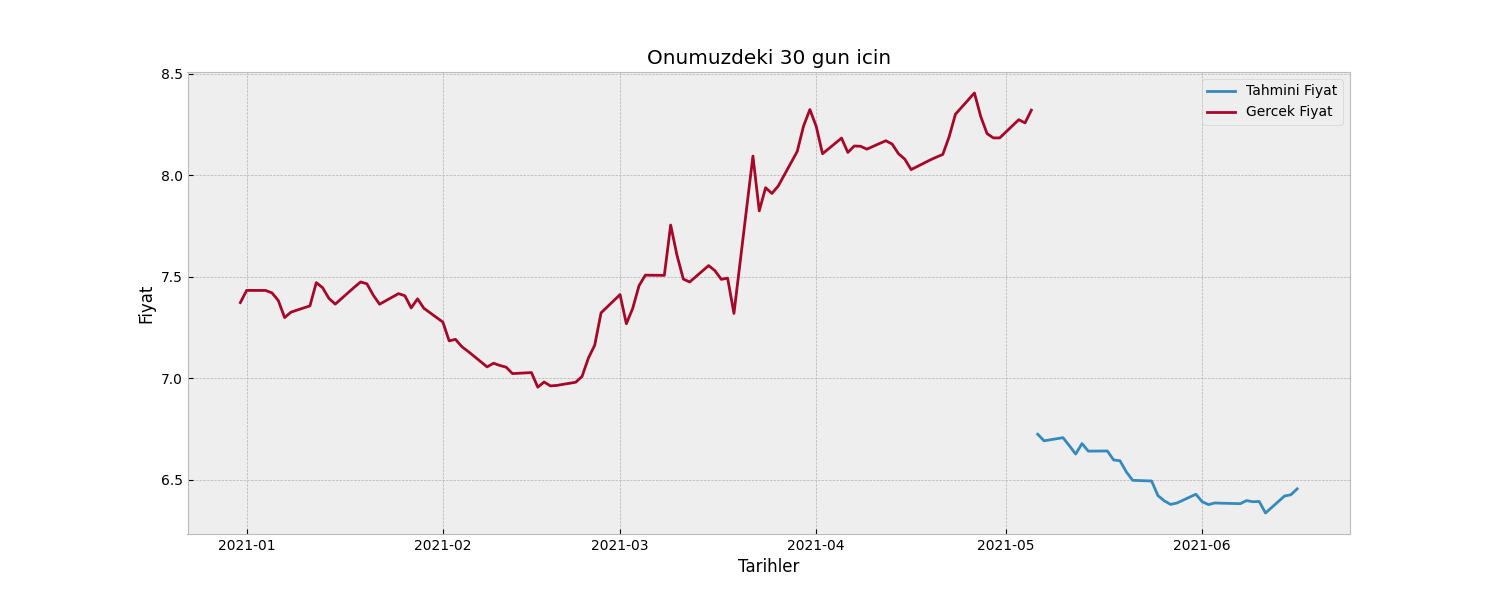

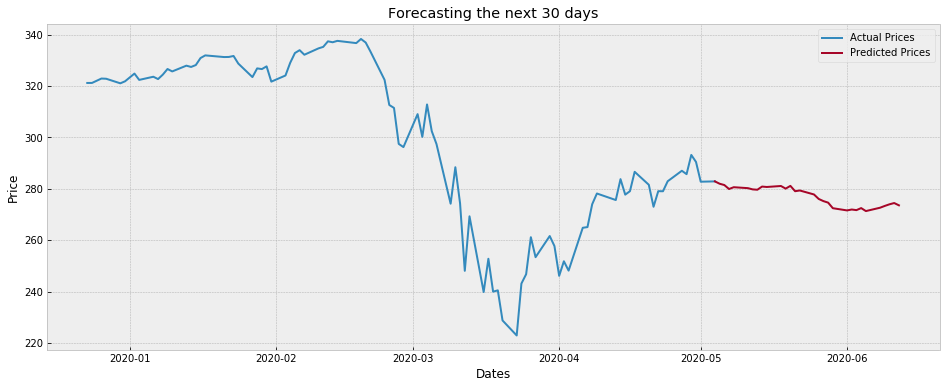

# Predicting off of the most recent days from the original DF

yhat = model.predict(np.array(df.tail(n_per_in)).reshape(1, n_per_in, n_features))

# Transforming the predicted values back to their original format

yhat = close_scaler.inverse_transform(yhat)[0]

# Creating a DF of the predicted prices

preds = pd.DataFrame(yhat,

index=pd.date_range(start=df.index[-1]+timedelta(days=1),

periods=len(yhat),

freq="B"),

columns=[df.columns[0]])

# Number of periods back to plot the actual values

pers = n_per_in

# Transforming the actual values to their original price

actual = pd.DataFrame(close_scaler.inverse_transform(df[["Close"]].tail(pers)),

index=df.Close.tail(pers).index,

columns=[df.columns[0]]).append(preds.head(1))

# Printing the predicted prices

print(preds)

# Plotting

plt.figure(figsize=(15,6))

plt.plot(preds, label="Tahmini Fiyat")

plt.plot(actual, label="Gercek Fiyat")

plt.ylabel("Fiyat")

plt.xlabel("Tarihler")

plt.title(f"Onumuzdeki {len(yhat)} gun icin")

plt.legend()

plt.show()Merhabalar,

Elimde bu şekilde bir kod var. Kodun mantığını kabaca anladım. Fakat gelecek günkü tahminlerde grafikte bozulma oluyor(Screenshot by Lightshot). Dolar ile alakası yok. BTC EUR filan hepsinde oluyor aynı şey. Kur geçmişini yahoo finance den alıyorum.

Kodun orijinal hali burada (Price-Forecaster/Stock-RNN-Deep-Learning-TechIndicators.ipynb at master · marcosan93/Price-Forecaster · GitHub)

Bu sayfadaki " Validating the Model" kısmından hata verdiği için plt.xlim('2018-05', '2020-05') burayı çıkarttım ve çıkarttıktan sonra hata vermemeye başladı. Bu hatayı verdiği yer “tahmin ve gerçek fiyat” grafiği, “gelecek günkü tahmin” grafiği ile alakası yok gibi ama sizce grafikteki problem burayı çıkarttığım için mi oldu ? Sizce grafikte bozulma neden oluyor ve nasıl düzeltebilirim ?